You deserve to build a life where money is a tool, not a constant alarm bell in your head.

If you grew up in a household where every purchase was weighed, debated, and sometimes regretted, you don’t just “move on” when you become an adult with your own paycheck.

Money becomes a feeling, a reflex, and a background noise in your head.

Here’s the tricky part: Even when you’re doing fine now, your nervous system might still act like you’re one unexpected bill away from disaster.

I’ve seen this from both sides. I spent years working with numbers as a financial analyst, and I’ve also watched how money stress shapes people’s habits, relationships, and self-worth in ways they don’t always notice.

Let me ask you something: When you spend money, do you feel calm or do you feel something else?

If “something else” rings a bell, here are seven signs you might have been shaped by a tight-money upbringing, plus what you can actually do about it:

1) You feel guilty buying anything that isn’t “necessary”

You can pay your bills yet, still, buying a simple treat can feel weirdly heavy.

Maybe you grab a fancy coffee and immediately think, “That could’ve been groceries,” or you finally replace a worn-out pair of shoes and feel the urge to justify it to someone who isn’t even there.

A tight-money childhood teaches you that “extras” are dangerous.

Even when you can afford them, your brain may tag them as irresponsible.

What helps is redefining “necessary.”

Joy is a need too, rest is a need, and feeling like a human—not a survival machine—is a need.

Try this: Create a tiny “no-explanation fund,” even if it’s small.

The rule is you’re allowed to spend it on something that makes your life sweeter without defending it in court.

2) You obsessively track prices and hate paying full price

Do you ever feel a mini rush when you get something on sale, and a mini sting when you don’t?

If you grew up watching every dollar, your brain learned to scan for threat and opportunity at the same time.

Price-checking becomes automatic.

I’ve talked to people who can remember the cost of milk from three different stores but can’t remember the last time they felt relaxed.

Here’s the cost of constant deal-hunting: Mental energy.

Savings matter, sure, but so does peace.

A helpful question is: Am I saving money, or am I buying relief?

If it’s relief, that’s a clue you’re still soothing an old fear.

A practical boundary: Pick a few categories where you bargain hunt guilt-free, and a few where you stop.

For example, compare grocery prices, but stop spiraling over a $12 item that solves a problem in your life.

3) You struggle to spend money on yourself but will spend on others

You might hesitate to buy yourself something simple, but you’ll happily treat your friend, cover the group dinner, or splurge on gifts.

Why? For many kids who grew up with scarcity, spending on yourself feels selfish.

Spending on others feels safer because it earns approval, proves you’re not “wasting” money, and feel like protection, like you’re making sure the people you love don’t feel the kind of stress you felt.

Generosity is beautiful, but if it leaves you resentful, anxious, or quietly struggling then it’s self-erasure in a cute outfit.

A quick reality check: If your budget is a home, are you furnishing everyone else’s rooms while sleeping on the floor?

Try setting a “matching” rule: If you spend $30 treating someone, you spend $30 on your own well-being within the week.

4) You feel restless unless you’re “being productive”

In tight-money homes, being idle can feel unsafe.

A lot of people pick up the belief that worth equals output.

If you’re not grinding, you’re falling behind; if you rest, you’re tempting fate.

It’s just a buzzing discomfort when you stop moving.

Even hobbies can turn into work as your brain whispers, “Could this make money? Should this be monetized?”

I’m all for competence and ambition but, when rest feels like danger, it’s often a leftover survival response.

I love this line from Anne Lamott: “Almost everything will work again if you unplug it for a few minutes, including you.”

If rest makes you anxious, start smaller than you think you need to.

Ten minutes of real downtime of no scrolling and no errands disguised as “relaxing,” then notice what comes up.

The goal is to teach your body that nothing terrible happens when you pause.

5) You avoid talking about money, even with people close to you

Some households talked about money constantly, but only in a stressful way.

Others didn’t talk about it at all, except in tense whispers.

Either way, you may have learned that money conversations lead to conflict, shame, or fear.

As an adult, you keep it vague.

You don’t ask what things cost, you don’t say what you earn, and you feel awkward discussing budgets, debt, even financial goals.

That can quietly sabotage relationships because money doesn’t stay out of relationships just because we avoid the topic.

It shows up as assumptions, resentment, power imbalances, and unspoken expectations.

If you want a simple way in, try using neutral language: “I’m trying to be more intentional with my spending. Can we talk about what feels comfortable for us?” or “I get anxious about money talks, but I want us to be on the same team.”

6) You hoard “just in case” items and hate throwing things away

Ever held onto a drawer full of random cords, takeout containers, or clothes that don’t fit, because you might need them someday?

When you’ve lived through not having enough, your brain builds safety through stockpiling.

Throwing something away can feel like tempting scarcity.

I’ve seen people keep items they actively dislike because getting rid of them feels like disrespecting the fact that they have them at all, but holding onto everything can become its own kind of stress.

A gentle way to work with this is to separate the fear from the object.

Instead of asking, “Do I need this?” ask, “What am I afraid will happen if I don’t have this?”

Give yourself a middle option afterwards: Keep one of the thing, not seven, or take a photo and let the item go, or set a “quarantine box” where you place items you think you might need, seal it, and revisit it in 30 days.

You’re building trust with yourself, and that’s the real goal.

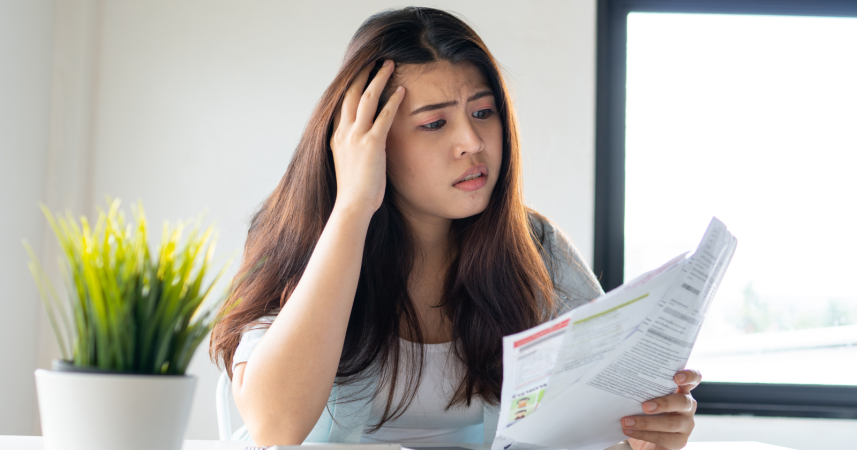

7) You over-prepare for disaster and struggle to feel financially safe

This is the biggest one, in my opinion.

Some people who grew up with money stress become extremely careful adults: Emergency fund, backups for backups, spreadsheets, insurance, contingency plans.

Still, they don’t feel safe.

They might think, “If I just hit a certain number, I’ll relax,” but then the number moves or the anxiety stays.

The fear isn’t always about math.

When money was tight, “unexpected” meant real consequences.

It meant adults panicking and instability, so your body learned that calm is temporary.

This is where it helps to define what “safe” actually means for you, in concrete terms.

Safe could be:

- I can cover my basics for three months if I lose income.

- I have a plan for medical or family emergencies.

- I know where I can cut spending without chaos.

- I have someone I can talk to if things get hard.

Then practice saying, out loud if you can: “Right now, I am okay.”

It might feel cheesy, but do it anyway!

You’re training your nervous system, not arguing with it.

Final thoughts

If you recognized yourself in a few of these, you’re adapted.

These patterns often start as smart survival skills; the problem is they don’t automatically update when your life changes.

Here’s a question worth sitting with: Which of these habits protects you, and which one limits you?

Pick just one sign that hit home and try one small shift this week, just a gentle update.

You deserve to build a life where money is a tool, not a constant alarm bell in your head.

What’s Your Plant-Powered Archetype?

Ever wonder what your everyday habits say about your deeper purpose—and how they ripple out to impact the planet?

This 90-second quiz reveals the plant-powered role you’re here to play, and the tiny shift that makes it even more powerful.

12 fun questions. Instant results. Surprisingly accurate.