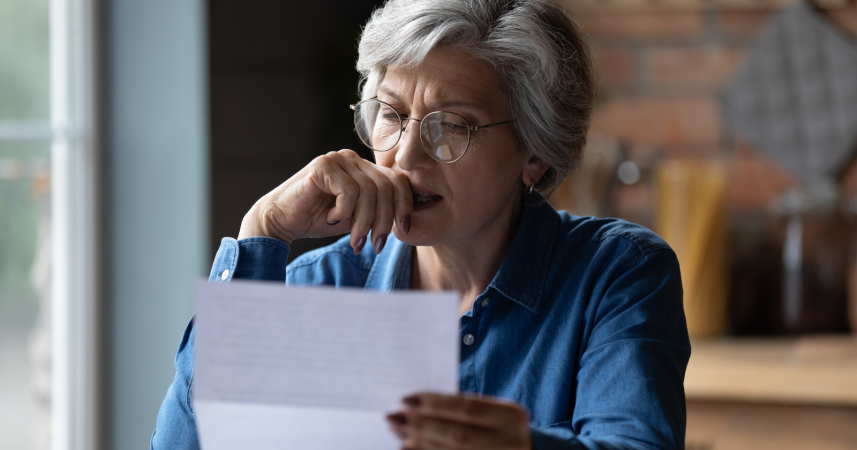

Three years after retiring with $420,000 and a paid-off house, I found myself at 3 AM filling out job applications for Home Depot while my wife slept upstairs, watching our "bulletproof" retirement plan crumble as inflation turned our careful 4% withdrawal rate into 8% just to maintain the same modest lifestyle.

![]()

Add VegOut to your Google News feed. ![]()

The moment I knew my retirement was broken came at 3 AM on a Wednesday, hunched over my laptop, searching "senior citizen job openings" while my wife slept peacefully upstairs.

Three years earlier, I'd walked away from 35 years in the restaurant business with $420,000 in the bank, thinking I'd cracked the code. Fifteen percent of every paycheck, saved religiously through divorce and downturns. The math was supposed to be bulletproof. Instead, I found myself filling out applications for Home Depot, wondering how I'd gotten the biggest calculation of my life so catastrophically wrong.

The numbers that were supposed to work

When I sold my restaurant at 58, every financial calculator on the internet told me the same story. Four hundred twenty thousand dollars, a paid-off house, modest spending habits — this was textbook retirement success. The advisor showed us colorful charts where our money grew even as we spent it. Four percent withdrawal rate, he said, like he was sharing the secret to eternal life.

I'd spent 35 years building to this moment. Started washing dishes at 16 in my uncle's diner, worked every station imaginable, eventually owned my own place for 18 years. Through all of it — the endless dinner rushes, the 2008 crash that nearly killed us, rebuilding after divorce — that 15% came off the top. Before groceries, before anything. It was sacred.

My wife Linda and I weren't planning yacht clubs and country estates. We wanted to cycle the lakefront trails, cook elaborate Sunday dinners for grandkids, maybe see Greece once. After decades of 70-hour weeks, the quiet felt earned. Year one was perfect. I did some restaurant consulting because I wanted to stay sharp, not because I needed the money. Mornings were for writing, afternoons at the farmers' market with my granddaughter, evenings on the back deck. The American Dream, achieved.

Then inflation arrived like a kitchen fire — sudden, consuming, and completely out of control.

When comfortable becomes catastrophic

The grocery receipts told the story first. Our usual $150 weekly shop became $180, then $220. Property taxes jumped 18% in one assessment. The gas bill doubled. When Linda needed dental work — nothing fancy, just necessary — insurance covered almost nothing of the $8,000 bill.

Our careful 4% withdrawal rate became 6%, then 8%, just to live the same life. No upgrades, no luxuries, just the same groceries and utilities and basic maintenance. The advisor's projections might as well have been written in crayon.

By year two, I was checking our investment balance obsessively, watching it drain while prices climbed. I'd managed restaurant chaos for decades, but this was different. There was no busy season coming to save us, no rush that would eventually end. Just the slow, relentless squeeze of expenses rising faster than any reasonable person could have predicted.

The math became simple and terrifying: at this rate, we'd be broke by 75.

The orange apron reality

The breaking point hit when our car needed $3,500 in repairs the same month we discovered the roof was leaking. Sitting at the kitchen table with my calculator, I finally understood that all those years of discipline meant nothing if inflation could erase them this quickly.

Linda found me at 2 AM filling out the Home Depot application. The shame was overwhelming — not at the work itself, but at the failure. I'd been a successful business owner, someone who'd built something real. Now I was applying to stock lumber because the alternative was financial ruin before we turned 70.

Twenty hours a week in the lumber department. That first day, wearing that orange apron, I ran into a regular from my old restaurant. His expression — surprise mixed with something worse, maybe pity — nearly sent me home. But I showed up the next day, and every day after, because pride is a luxury people with draining bank accounts can't afford.

The retirement nobody talks about

Here's what nobody tells you: inflation in retirement isn't just mathematical. It's psychological warfare. You watch your carefully constructed future dissolve in real-time while the world keeps insisting you should have saved more, invested better, seen it coming.

My cycling group became a support group for the retirement betrayed. Former teachers substituting again, managers working overnight security, professionals who'd followed every rule now scrambling for part-time work. We'd all bought the same lie about what $400,000 or $500,000 or even $600,000 could do.

The young people at Home Depot don't care that I used to own a restaurant. They just know I show up on time and can explain the difference between pressure-treated lumber and cedar. There's unexpected dignity in that simplicity, in being useful without the weight of what you used to be.

We adapted because that's what you do. I expanded my consulting, started teaching cooking classes at the community center, took on more hours at the store. Linda went back to work too. Greece became local road trips. The organic farmers' market became regular grocery stores. We downsized dreams to fit our new reality.

What saving for 35 years actually bought me

Sometimes I think about all those Friday nights I stayed in, all those vacations we didn't take, all those times I said "we're saving for retirement" when Ethan wanted something expensive. I wonder what would've happened if I'd known the future would cost twice what I'd saved for.

The truth is uncomfortable: the system broke its promise. We did everything they said — worked hard, saved consistently, invested conservatively, avoided debt. But inflation doesn't care about your discipline. It's a force that reveals how vulnerable even the prepared actually are.

I still save, even now at 62, working retail. Not because I believe it'll be enough — that innocence is gone — but because not saving feels like complete surrender. Every Friday, I cash my Home Depot check and put aside what I can. It's not 15% anymore, but it's something.

When customers recognize me from the restaurant days, I used to scramble for explanations. Now I just say, "Making it work, like everyone else." Because that's what this is — not the retirement we were promised, but the one we got, and we're all just trying to make it work.

Final words

My grandkids don't care that their grandfather stocks lumber now. They care that I still make them Sunday pizzas, still read stories with all the voices, still take them for ice cream. Maybe that's the only retirement that actually matters — the moments between whatever work keeps you afloat.

I'm not bitter, exactly. Disappointed at a system that pretended $420,000 was wealth while knowing inflation would devour it. Tired of the constant calculations and anxiety. But mostly, I'm still here, still working, still adapting. The restaurant kitchen taught me that when everything's on fire, you don't panic. You just keep moving, one task at a time.

Tomorrow, I'll put on that orange apron again. Not because it's what I planned, but because it's what needs doing. And maybe that's the most honest retirement advice I can give: forget the calculators and projections. Save what you can, work as long as you're able, and find dignity in whatever keeps you going. The future costs more than anyone tells you it will.

What’s Your Plant-Powered Archetype?

Ever wonder what your everyday habits say about your deeper purpose—and how they ripple out to impact the planet?

This 90-second quiz reveals the plant-powered role you’re here to play, and the tiny shift that makes it even more powerful.

12 fun questions. Instant results. Surprisingly accurate.